Presenters

James Peyer, Cambrian Bio

James Peyer is the Chief Executive Officer and Co-Founder of Cambrian Biopharma. He also serves as the Chairman of the Board of Sensei Biotherapeutics and board and executive roles across Cambrian’s pipeline. He has spent his…

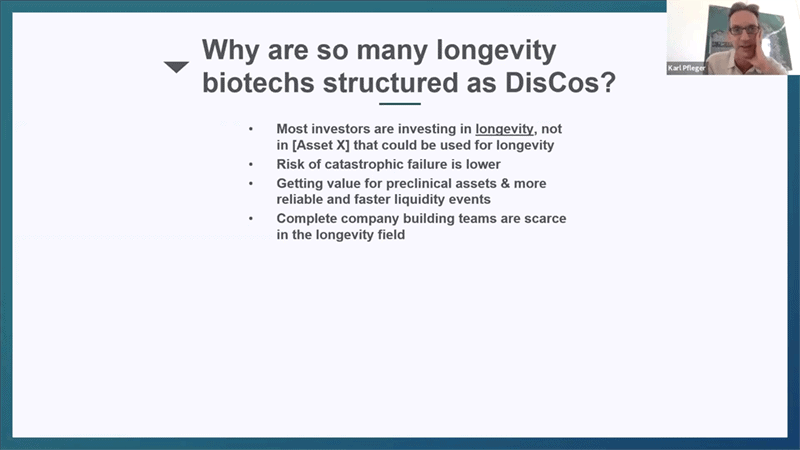

- Cambrian is a DisCo (Distributed Drug Discovery Company) structure, so a single biotech that acquires and develops other biotechs underneath us. So not quite a company building studio, not a traditional pharmaceutical company, definitely not a VC, but a kind of mixture of all of those three things.

How to think about longevity biotech

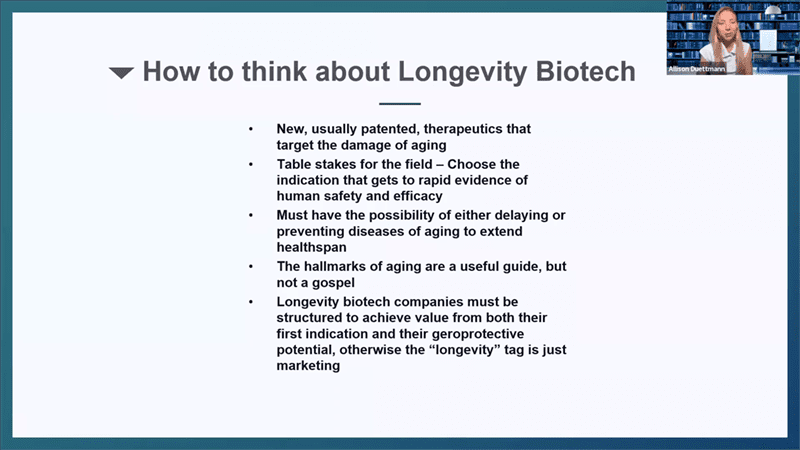

- What actually defines a longevity biotech company? I define it as private companies, almost always for profit, that are taking new usually patented therapeutics that target the damage of aging. And that’s the key, it doesn’t matter what’s the first indication, usually it is not directly aging at first, but it needs to target the underlying damage of aging. At Cambrian, we also have an extra caveat that it also must be at least in theory possible to turn it into a preventative drug – so it should be at least in theory possible to use it in healthy person and prevent them from getting sick instead of waiting for them to get sick and then try to unwind that.

- Tablestakes around indication selection. Before 2015 or so, longevity biotech was kind of described as the people who want to do clinical trials in healthy older people to slow down aging and I think that’s not the investible moat for this field. The way the industry is shaping up right now is that if you have a molecule that can target the damage of aging, people are choosing whichever indication or disease that gets the most rapid evidence of human safety and efficacy. And once you have that, the presumption is that you can take this drug and run a clinical trial in healthy people and prevent them from getting sick.

- Cambrian and most of the other multi-asset companies have organized themselves around the hallmarks of aging as the main organizing principle. Hallmarks are a useful guideline, but are really not a gospel, so we don’t spend a lot of time inquiring directly about which hallmarks specific drugs target – I think that’s an unhelpful way to think about it. Hallmarks of aging basically bundled all the different competing theories of aging because there was sufficient evidence that no one of those theories were sufficient to explain all of the data that we were starting to get about extension of mammalian lifespan, therefore elements of all of these things had to be true.

- Longevity biotech companies must be structured to achieve value both from their first indication and then from their geroprotective potential later, otherwise the longevity label is just marketing. Most biotechs are built to get bought in their late clinical stages. With the current approach of getting approached by big pharma companies in later clinical trial stages, if the companies do not structure their trials in a way that goes towards the geroprotective potential, they will fail and not deliver on their longevity promise. The chances that the big pharma company will run the geroprotective trial is nearly zero. So unless you’re setting up the company to be sustainable enough to make decisions about which trials to run after the first approval of the drug, it’s not really gonna have a big impact on the geroscience space.

What is DisCo?

Barriers preventing us from starting clinical trials with the first geroprotectors

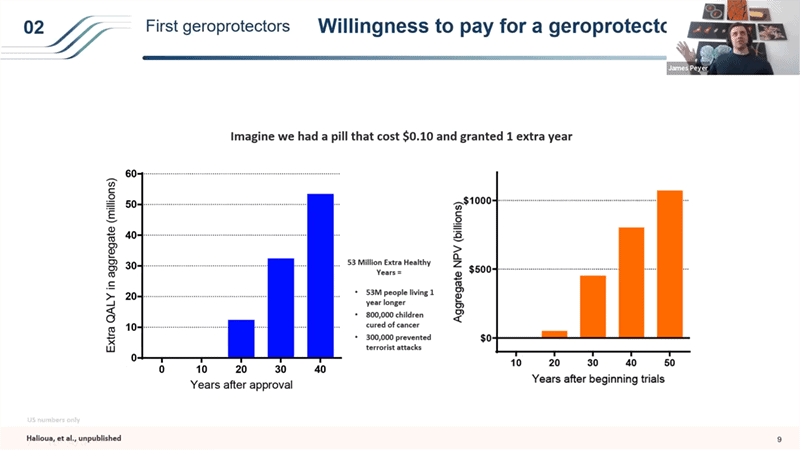

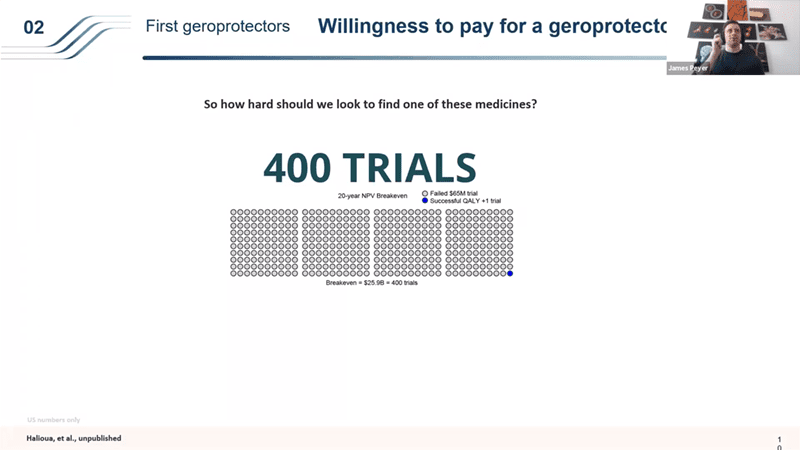

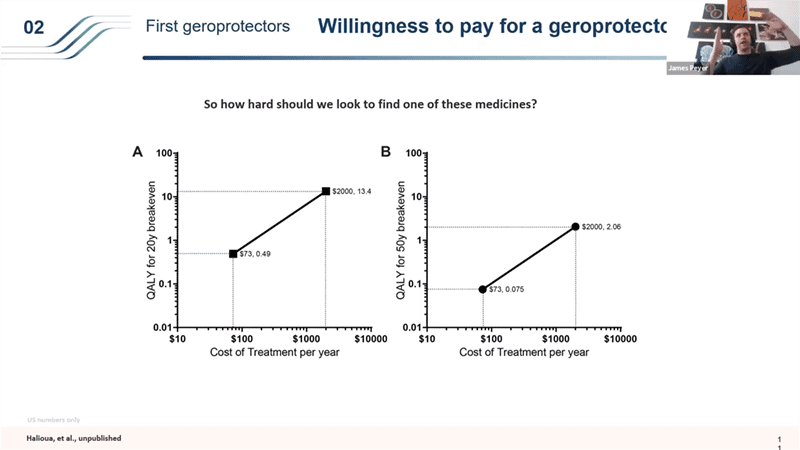

- So if you take the same 20 year timeframe where you have to get your money back for society in the first 20 years of setting up a bunch of different trials, if you have a drug that costs like a $70 a year like Metformin, the threshold for breaking even for the investment you make to distribute and get this drug into millions and millions of people is very low. Anything over 0.4 extra QALYs (so shifting lifespan from 80 to 80.4 years), if you do better than that, it is worth it as an investment for society. But it’s a very price sensitive structure that people don’t usually think about. Because you’re treating people for so many years before you see the benefit of this, if you increase the price to $2000 a year, (which is interestingly about what Lipitor cost – statins when they are under a patent cost around that price), the bar becomes so much higher for that breakeven point – you would need to be delivering more than 13.4 extra QALYs to be break even within the first 20 years (if you have 10 years long clinical trials). And that then changes dramatically if you have shorter time frames in the clinical trials or longer timeframes for the break even point.

- The point that I wanted to bring up with this is why it is so important to start with generics – this price element plays a huge role in how a drug like this would get rolled out. So these philanthropic trials with generics can set a very nice bar for us and as soon as you lower the clinical trial timelines using those generics, then it changes the models dramatically and we can start running these patented drug trials in the 2030s.

- It is a powerful way to look at the topic. Also Andrew Scott has recently published a great paper using the “willingness to pay” metric.